by: Lana Clements

- 0

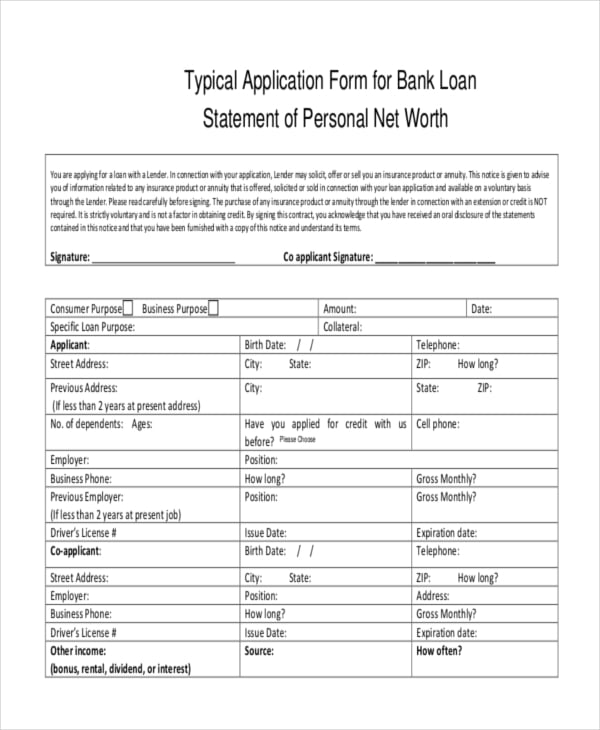

Regulating rules from the Monetary Conduct Authority (FCA) do not identify you to definitely bank statements must be used to evaluate affordability, however, lenders will make use of them to ensure money, and additionally outgoings.

However some banking companies features unofficially went from this approach and is actually instead depending on credit rating, among almost every other mode, to evaluate appropriate borrowers.

The bank extra when expected to transmit an announcement to be certain that, including, gurus or income, advisors is simply post the newest single page on which money entry try presented.

Bank comments create underwriting troubles

Financial statements provide all sorts of more issues when you look at the an application, that is the reason certain lenders may avoid deciding on him or her, advisors suggested.

Nick Morrey, equipment technology movie director during the broker John Charcol, said while some lenders never inquire about statements, they may not be fundamentally advertisements so it.

The guy extra: What they want to see firstly would be the fact the latest income announced into payslip is really what goes in new checking account, which can be readable to have potential con causes.

But once he or she is thinking about a lender declaration they have to examine they safely and therefore means deciding on most of the deals to see if there can be something that the financial institution could see given that problematic.

Malcolm Davidson, managing movie director on large financial company British Moneyman, questioned whether or not loan providers really want to be aware of the whole insights about prospective borrowers.

Rachel Lummis out-of Xpress mortgage loans told you regardless of if loan providers will most likely not ask for new records, it isn’t a beneficial get free from prison card‘ having borrowers.

She added: The newest agent requires lender comments to possess examining value, demonstrating money and you will compliance aim additionally the financial totally needs the fresh agent to have her or him with the document.

She told you: No matter whether the lender requires a lender statement, I am able to however obtain three months to add to my personal file.

I’d an instance simply recently where We examined my clients lender statements and he got over fifty gaming transactions in the a couple of months period.

We caused it to be clear with the client that he risked getting refused when your lender had a problem with him or her.

In addition ensured which i allocated ?600 towards the their budget, and when the guy continued the latest routine. The mortgage had alright, not my conformity notes ensured this particular issue was showcased and i had considered brand new perception regarding the.

The lower the loan to worth, brand new faster documents typically required by the lender… Nevertheless doesn’t mean the adviser doesn’t need to carry out the work of one’s financial by barbecuing clients and having an excellent a good compliant document so you can ring-fence every thing.

There is no requirements you to definitely a broker need to request bank comments out of a borrower given that evidence of cost, but just like the advisers indexed it can render proof of brand new viability from required product sales.

The lending company is in charge of complying on regulator’s financing laws and regulations and you can making sure the fresh new debtor find the money for pay the borrowed funds.

Out-of kilter with Discover Banking

Sebastian Riemann, agent during the Libra Monetary Believe, said: Lenders can scrutinise all expenses habits and activities and it is likely that particular that would normally have certified, after that slip beyond lenders requirements.

Davidson advised to avoid lender comments was from kilter on the notion of Discover Financial and you will requested just how these lenders usually are employed in the new ecosystem.

He told you: Discover banking is about to bring about which slicker home loan processes however, lenders don’t want to find [the consumers ingoings and outgoings].

A spokeswoman to have Santander told you: Brokers possess fed right back that there surely is often suspicion within the paperwork that’s important for for every single application, ultimately causing additional documentation are needlessly collated and you may registered.

To support him or her, i sent an e-post making clear the latest documentation criteria one part of this was doing securing applicant’s lender statements.

Given that a prudent lender, we need to usually make sure the necessary value inspections are performed to ensure that some one have the merchandise that match their requirements and you may are able to afford the mortgage into the duration of the word.

The newest communication was designed to help brokers assemble that was expected having unique circumstances, helping them to easily and quickly get the correct choices getting the consumer.

We have now gain access to customers information regarding credit agencies, which can only help color a picture of people, in addition to current membership turnover included in automated earnings verification.

I greeting any more pointers that Unlock Banking can bring, our very own concern are help brokers and you can making sure people get the proper home loan to meet up with their requirements.

An effective spokeswoman for Halifax said it will not inquire about lender statements as loan providers explore numerous gadgets to assess a customer’s mba student loan interest rates credit history, plus credit scoring and a cost evaluation.

Of a lot loan providers verified they actually do however require bank comments, regardless if NatWest has no need for comments in case your debtor has already been good consumer.

A spokesperson to possess Accord Mortgage loans told you: We want at least one financial statement as part of our mortgage application process to have the ability to validate the accuracy and you can authenticity from a beneficial borrower’s income.

As we take note of a potential borrower’s outgoings, i get it done in the interests of the borrower and you may ourselves to ensure he’s got the ability to be able to settle the arranged payment.

Like, we see lingering economic duties, that will imply a personal debt cost strategy which had been in past times undeclared, or whether or not applicants are regularly incapable of escape the overdraft or whether around people signs and symptoms of people staying in monetary challenge.

Podobné články

Play casino hello 25 free spins 777 Online Slot Games That have 250% Bonus

Play casino hello 25 free spins 777 Online Slot Games That have 250% Bonus Nine Casino 50 totally free spins extra no deposit needed

Nine Casino 50 totally free spins extra no deposit needed Spinbetter Casino Bonus Za Registraci

Spinbetter Casino Bonus Za Registraci Kostky V Kasinu

Kostky V Kasinu Sportwetten bloß Mindesteinzahlung Nicht früher als 1 Maklercourtage möglich

Sportwetten bloß Mindesteinzahlung Nicht früher als 1 Maklercourtage möglich Ruleta Video

Ruleta Video Da Vinci Expensive diamonds Twin Enjoy Ports Play for totally free now! Zero obtain required

Da Vinci Expensive diamonds Twin Enjoy Ports Play for totally free now! Zero obtain required